Based on contractor experience, homeowner communication, supplement flexibility, inspection quality, and overall claim handling.

This is obviously opinion-based, but after working thousands of roof claims in Texas through Texas Professional Roofing, patterns absolutely emerge. Some carriers communicate well, inspect fairly, and work with homeowners to resolve legitimate storm damage claims. Others create delays, deny obvious damage, or make the process unnecessarily difficult.

1. USAA — Best Overall for Policyholders

USAA is usually one of the easiest carriers to work with when the policyholder has solid coverage.

What They Typically Do Well

- Strong communication

- Faster response times

- Better customer service

- More reasonable supplement handling

- Easier to reach adjusters

- Better homeowner experience overall

Challenges

- Like all carriers, they’ve become stricter in recent years

- Deductibles are often high

- Some older roofs may move toward ACV settlement structures

Still, from a contractor and homeowner standpoint, they’re generally one of the most fair and organized carriers we deal with.

2. State Farm — Consistent and Process Driven

State Farm tends to be very process-oriented. If damage is there and documented properly, claims often move relatively smoothly.

Pros

- Usually reasonable inspections

- Supplements often reviewed fairly

- Good digital systems

- Adjusters typically communicate

Cons

- Can become strict on borderline claims

- Sometimes slow on supplement approvals

- Documentation requirements continue increasing

Overall, still one of the more workable large carriers.

3. Farmers Insurance — Mixed but Often Manageable

Farmers can vary heavily depending on the adjuster and policy type.

What We See

- Older roofs often pushed toward ACV policies

- More scrutiny on aging roofs

- Some adjusters are excellent, others extremely conservative

Positive Side

- Once approved, claims can move fairly well

- Communication is usually better than some competitors

- Supplements are often negotiable if properly documented

4. Liberty Mutual / Safeco — Increasingly Difficult

These carriers have become noticeably tougher over the past few years.

Common Issues

- Higher hail hit thresholds

- More denials on borderline roofs

- Heavy documentation requirements

- Increased use of engineering reports

Many contractors across Texas have noticed a significant tightening in approvals.

5. Travelers — Contractor Program Heavy

Travelers often pushes homeowners toward their preferred contractor network.

What Homeowners Should Know

- You are NOT required to use their contractor

- Their initial estimates are often low

- Supplements are frequently needed

- They can be very pricing-controlled

That doesn’t mean claims cannot get approved, but homeowners often need a contractor experienced in supplements and scope review.

6. Allstate — Most Difficult Overall

In our experience, Allstate has consistently been one of the hardest carriers to work with on roof claims.

Common Issues We See

- Frequent denials on legitimate storm damage

- Communication challenges

- Heavy reliance on third-party inspectors

- Long delays between inspections and decisions

- Low initial scopes

- Offsite desk adjusters making decisions without fully understanding the roof condition

Biggest Frustration

Many homeowners feel like they cannot get direct answers. Communication often becomes fragmented between field inspectors, desk adjusters, and third-party reviewers.

Even when damage is obvious, the process can become drawn out and frustrating for the policyholder.

Important Reality Homeowners Should Understand

No insurance company is “easy” anymore.

Texas carriers have tightened significantly after years of major hail losses and rising claim costs. Even good carriers are:

- scrutinizing claims harder

- increasing deductibles

- shifting toward ACV policies

- requiring more documentation

- using engineers more frequently

That’s why proper inspections, photo documentation, and contractor experience matter more than ever.

Biggest Advice to Homeowners

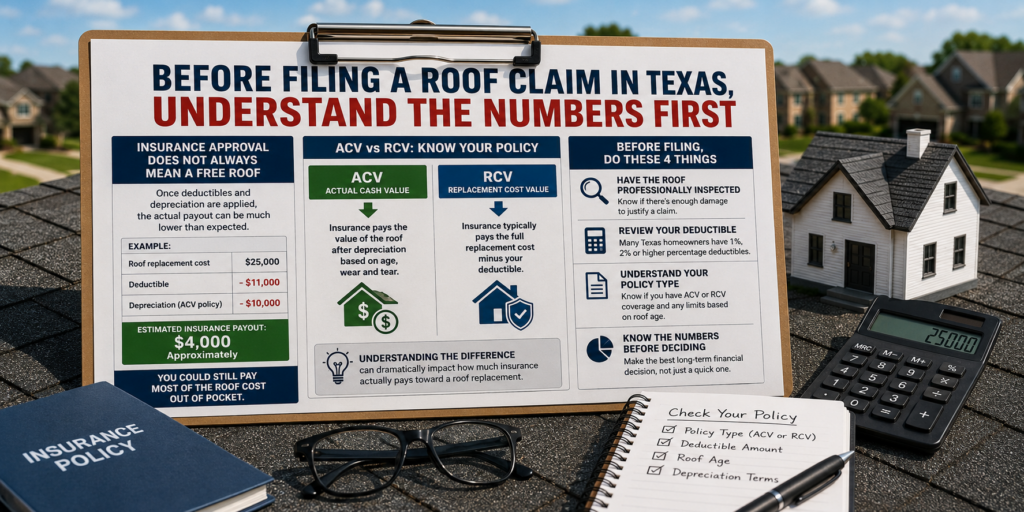

Before filing a claim:

- Have the roof professionally inspected first

- Verify there is actually enough storm damage

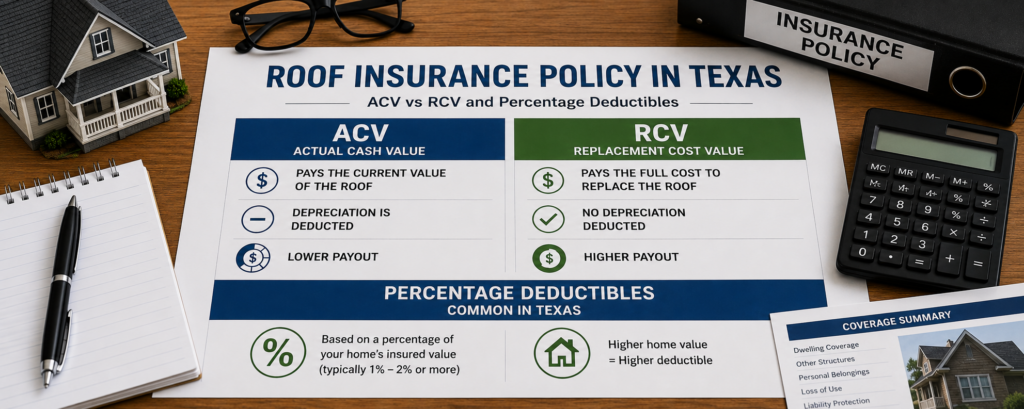

- Understand your deductible and policy type (RCV vs ACV)

- Avoid contractors pushing claims without evidence

- Work with someone experienced in supplements and adjuster meetings

A bad claim filing on a borderline roof can create issues later when a legitimate storm hits.

Final Thoughts

The best insurance companies:

- communicate clearly

- inspect fairly

- explain decisions

- work toward resolution

The worst ones tend to:

- delay communication

- outsource inspections heavily

- under-scope claims

- create friction during supplements

- deny borderline but legitimate damage repeatedly

For homeowners in Texas, the carrier you choose absolutely affects your experience when storm season hits.